11

11

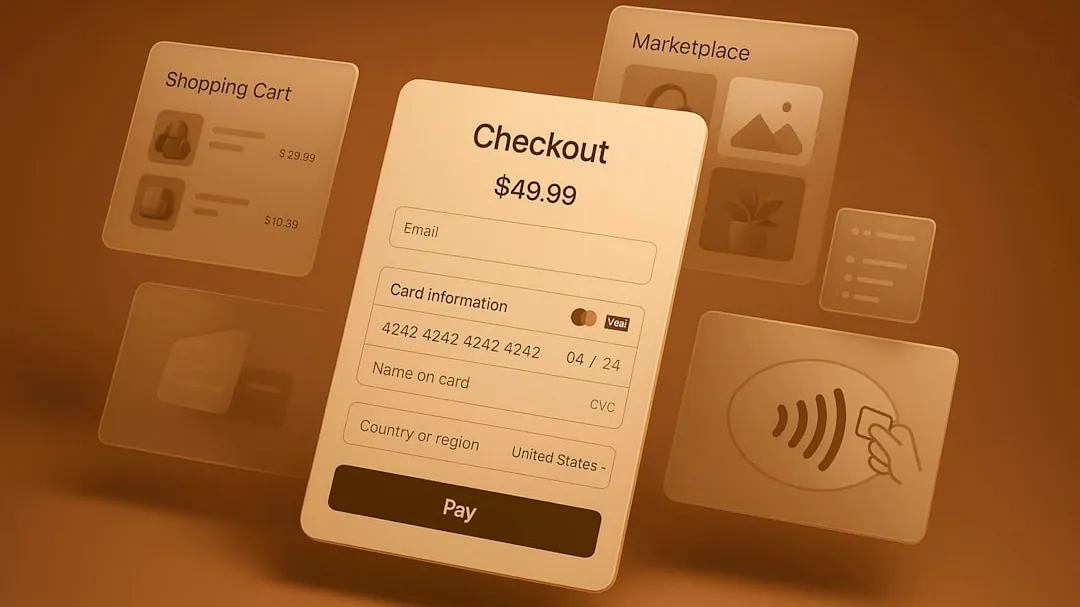

Visa’s Intelligent Commerce Connect is not an experiment in generative agents — it’s a payment infrastructure play that lets third‑party AI agents transact on behalf of users by tying card rails to a variety of agent protocols and blockchain payment standards. For merchants and payments teams, the concrete implication is a new integration and compliance calculus: accept agent-driven checkout now through Visa’s stack, keep supporting crypto-native rails, or run parallel flows while regulators and consumers decide which wins.

Intelligent Commerce Connect presents itself as a protocol-agnostic on‑ramp: a single integration on the Visa Acceptance Platform that supports AI agent protocols such as the Trusted Agent Protocol, Machine Payments Protocol (MPP), Agentic Commerce Protocol (ACP), and Universal Commerce Protocol (UCP). Visa also integrated Coinbase’s x402 crypto payment protocol via a strategic partnership with AI fintech Nevermined; Visa’s announcement cites x402’s early traction — roughly $24 million processed over a 30‑day stretch — to underline practical interoperability between blockchain and traditional rails.

Operationally this means merchants can make product catalogs discoverable to agent platforms without building separate gateways for each agent protocol. Visa says the platform will handle payment initiation, tokenization, and orchestration for enablers processing on merchants’ behalf, while remaining compatible with both Visa and non‑Visa cards to broaden reach beyond pure Visa ecosystems.

The architecture emphasizes transaction-level controls that change how merchant risk looks when an autonomous agent pays: dynamic tokenization protects card data, granular spending controls let end users set budgets and merchant blacklists, and contextual authentication evaluates risk in real time. Visa also manages PCI‑level compliance and orchestration for third‑party enablers, which reduces one operational burden for merchants but pushes new expectations onto payments teams about configuring and enforcing agent rules.

Visa’s rollout plan — pilots across Asia‑Pacific, Europe, and the Middle East now, a developer beta in Q3 2025, and general availability for banks and large merchants by Q1 2026 — signals a phased approach. That timetable reflects explicit attention to regulatory questions (liability and consumer protection) and system resilience; merchants should treat the platform as a guarded expansion of their payment surface rather than an immediate replacement for existing flows.

Payments teams face three concrete trade‑offs: integration complexity, control over the checkout experience, and settlement/fee paths. A single Visa Acceptance Platform integration centralizes agent orchestration and PCI handling, but it routes agent interactions through Visa’s policy and processing stack. Crypto‑native options like x402 or MPP may preserve different settlement mechanics and allow agent-to-agent native-token flows, at the cost of extra on‑ramp and compliance work for merchants and acquirers.

| Decision dimension | Visa Intelligent Commerce Connect | Crypto-native protocols (x402, MPP) |

|---|---|---|

| Integration | Single integration via Visa Acceptance Platform; PCI orchestration handled | Separate on‑ramps and gateway work; direct blockchain settlement options |

| Control & security | Dynamic tokenization, granular spending controls, contextual auth | Protocol-level cryptographic assurances; merchant must manage wallets/bridges |

| Cross-border & CBDC readiness | Roadmap includes CBDC support and cross-border commerce capabilities | Depends on protocol adoption and bridge infrastructure; faster native token moves |

| Timing & risk | Pilot → developer beta (Q3 2025) → GA (Q1 2026); regulatory scrutiny anticipated | Already active in some agent flows (x402 traction reported); legal clarity varies by jurisdiction |

Merchants and acquirers should treat Intelligent Commerce Connect as a conditional option: pilot if a meaningful share of traffic already comes via AI‑assisted discovery or if your checkout experience can be adjusted to surface agent‑specific controls. Key checkpoints before broad rollout are (1) regulatory guidance on merchant liability and consumer consent in your jurisdiction, (2) measurable consumer adoption — not just marketing interest — in agent checkout flows, and (3) pilot results showing fraud and chargeback rates at or below existing benchmarks.

When will this matter operationally? If you have pilots or partners experimenting with AI agents now, integrate in pilot mode ahead of the Q3 2025 developer beta; larger rollouts should wait for GA in Q1 2026 and clearer regulatory signals.

Does Visa create the agents? No. Visa provides the payment plumbing and compliance controls; third parties build the agent logic and user consent rules.

What are red flags to pause adoption? Lack of consumer opt‑in, unresolved liability rules from local regulators, or pilot metrics showing elevated fraud or unexpected chargebacks — any of these warrant delaying full integration.

Disclaimer: CryptoBetInsight.com is an informational website only and does not operate or provide any online gambling services. Availability of gambling services depends on the laws and regulations of your jurisdiction. Users are solely responsible for ensuring that their use of any external service complies with local laws and regulations.

Affiliate Disclosure: Some links on this website may be affiliate links. If you sign up or make a purchase through these links, we may earn a commission at no additional cost to you.

Legal Compliance: Users from the United States and other jurisdictions must comply with all applicable federal, state, and local laws regarding online gambling. Where applicable, users must meet the legal age requirements in their jurisdiction (commonly 21+).

Responsible Gambling: Please gamble responsibly and only wager what you can afford to lose. If you believe you may have a gambling problem, consider seeking help from a local support organization or a responsible gambling resource.